DRS/A: Draft registration statement submitted by Emerging Growth Company under Securities Act Section 6(e) or by Foreign Private Issuer under Division of Corporation Finance policy

Published on February 3, 2023

As confidentially submitted to the Securities and Exchange Commission on February 3, 2023.

This draft registration statement has not been publicly filed with the Securities and Exchange Commission

and all information herein remains strictly confidential.

Registration Statement No. 333-[ ]

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________________

Form F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

_____________________________

DDC Enterprise Limited

(Exact name of Registrant as specified in its charter)

_____________________________

Not Applicable

(Translation of Registrant’s name into English)

_____________________________

|

Cayman Islands |

2000 |

Not Applicable |

||

|

(State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

Room 3-6, 4/F, Hollywood Center

233 Hollywood Road

Sheung Wan, Hong Kong

Telephone: +852-2803-0688

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

_____________________________

Cogency Global Inc.

122 East 42nd Street, 18th Floor

New York, NY 10168

+1-800-221-0102

(Name, address, including zip code, and telephone number, including area code, of agent for service)

_____________________________

Copies of all communications, including communications sent to agent for service, should be sent to:

|

Lawrence S. Venick, Esq. |

Stephanie Tang, Esq. 88 Queensway Road Hong Kong SAR |

_____________________________

Approximate date of commencement of proposed sale to public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act:

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Commission, acting pursuant to such Section 8(a), may determine.

____________

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

|

PRELIMINARY PROSPECTUS (SUBJECT TO COMPLETION) |

dated FEBRUARY 3, 2023 |

Class A Ordinary Shares

DDC Enterprise Limited

This is the initial public offering of our Class A ordinary shares (“Class A Ordinary Shares”). We are offering [ ] of our Class A Ordinary Shares, par value $[ ] per share, on a firm commitment basis. The estimated initial public offering price is expected to be $[ ] per share. Currently, no public market exists for our Ordinary Shares. We have applied to list our Class A Ordinary Shares on the [New York Stock Exchange, or NYSE/Nasdaq Capital Market, or Nasdaq], under the symbol “[ ]”. We cannot guarantee that we will be successful in listing our Class A Ordinary Shares on the Nasdaq; however, we will not complete this offering unless we are so listed.

We are both an “emerging growth company” and a “foreign private issuer” as defined under the U.S. federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements for this and future filings. See “Prospectus Summary — Implications of Being an Emerging Growth Company and a Foreign Private Issuer” for additional information. Investors are cautioned that you are buying shares of a shell company issuer incorporated in the Cayman Islands with operating subsidiaries in China and Hong Kong, investors will not hold direct equity investments in our China and Hong Kong operating subsidiaries. Our Class A ordinary shares offered in this prospectus are shares of our Cayman Islands holding company. See “Risk Factors — Risks Related to Doing Business in China and Hong Kong — Changes in China’s economic, political or social conditions or government policies could have a material adverse effect on our Company’s business and results of operations we may pursue in the future; — Uncertainties with respect to the PRC legal system, including uncertainties regarding the enforcement of laws, and sudden or unexpected changes in laws and regulations in China could adversely affect us; and — The Hong Kong legal system embodies uncertainties which could limit the legal protections available to us.”

We will not be a “controlled company” under the [New York Stock Exchange Listed Company Manual/Nasdaq Stock Market Rules] post public offering.

Investing in our Class A Ordinary Shares is highly speculative and involves a significant degree of risk. Our Class A ordinary shares offered in this prospectus are shares of our Cayman Islands holding company. Although “we,” “us,” “our” or “our company” refer to DDC Enterprise Limited and its subsidiaries and VIEs as a whole for ease of reference and discussion, investors should be aware that DDC Cayman and its subsidiaries do not have direct ownership in the VIEs, but rather exert control over and receive economic benefits from the VIEs through various contractual arrangements. In this prospectus where business activities or functions of the VIEs are described, specific references will be made to the relevant VIEs. We currently conduct our business through Shanghai DayDayCook Information Technology Co., Ltd, or SH DDC, and Shanghai Lashu Import and Export Trading Co., Ltd., or SH Lashu, each an indirect wholly owned subsidiary of DDC Cayman, and a number of operating subsidiaries non-wholly and wholly owned by SH DDC. All of these operating subsidiaries are established under the laws of the PRC. During the two years ended December 31, 2020 and 2021, we had conducted part of our operations in China through contractual arrangements with two variable interest entities and their consolidated entities (the “Weishi and City Modern VIEs”), namely, Shanghai Weishi Information Technology Co., Ltd., Shanghai City Modern Agriculture Development Co., Ltd., Shanghai City Vegetable Production and Distribution Co-op, Shanghai Jiapin Vegetable Planting Co-op, Shanghai Jiapin Ecological Agriculture Co-op. Through such contractual arrangements, we, through our indirect wholly-owned PRC subsidiary Shanghai DayDayCook Information Technology Co., Ltd., control and receive the economic benefits of the Weishi and City Modern VIEs without owning any direct equity interest in them. As of April 2022, such contractual arrangements with the Weishi and City Modern VIEs have been terminated. However, as at the date of this prospectus, we still have contractual arrangements with Chongqing Mengwei Technology Co., Ltd., Liao Xuefeng, Chongqing Changshou District Weibang Network Co., Ltd. and Chongqing Yizhichan Snack Food Electronic Commerce Service Department to enable us to have the ability to control a number of online stores purchased from them since the titles of such online stores cannot be transferred to us due to the limitations from the policies of certain online platforms. These online stores are considered VIEs and SH DDC is the primary beneficiary. We refer to these online stores the “Mengwei VIE” throughout this prospectus.

Recent statements by the Chinese government have indicated an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investments in China based issuers. Any future action by the Chinese government expanding the categories of industries and companies whose foreign securities offerings are subject to government review could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and could cause the value of such securities to significantly decline or be worthless.

Recently, the PRC government initiated a series of regulatory actions and made a number of public statements on the regulation of business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using a variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding efforts in anti-monopoly enforcement. As there remains significant uncertainty in the interpretation and enforcement of relevant PRC cybersecurity laws and regulations, we cannot assure you that we would not be subject to cybersecurity review or investigations launched by PRC regulators. On December 28, 2021, the Cyberspace Administration of China (the “CAC”), and 12 other relevant PRC government authorities published the amended Cybersecurity Review Measures, which came into effect on February 15, 2022. The final Cybersecurity Review Measures provide that a “network platform operator” that possesses personal information of more than one million users and seeks a listing in a foreign country must apply for a cybersecurity review. Further, the relevant PRC governmental authorities may initiate a cybersecurity review against any company if they determine certain network products, services or data processing activities of such company affect or may affect national security. As a network platform operator who possesses personal information of more than one million users for purposes of the Cybersecurity Review Measures, we have applied for and completed the cybersecurity review with respect to our proposed overseas listing pursuant to the Cybersecurity Review Measures. See “Risk Factors — We may be liable for improper collection, use or appropriation of personal information provided by our customers.” Because these statements and regulatory actions are new, however, it is highly uncertain how soon legislative or administrative regulation making bodies in China will respond to them, or what existing or new laws or regulations will be modified or promulgated, if any, or the potential impact such modified or new laws and regulations will have on our daily business operations or our ability to accept foreign investments and list on an U.S. exchange.

The Holding Foreign Companies Accountable Act, or the HFCAA, was enacted on December 18, 2020. In accordance with the HFCAA, trading in securities of any registrant on a national securities exchange or in the over-the-counter trading market in the United States may be prohibited if the Public Company Accounting Oversight Board (the “PCAOB”) determines that it cannot inspect or fully investigate the registrant’s auditor for three consecutive years beginning in 2021, and, as a result, an exchange may determine to delist the securities of such registrant. On December 23, 2022, the Accelerating Holding Foreign Companies Accountable Act, or the AHFCAA, was enacted, which amended the HFCAA by reducing the aforementioned inspection period from three to two consecutive years, thus reducing the time period before our

securities may be prohibited from trading or delisted if our auditor is unable to meet the PCAOB inspection requirement. Pursuant to the HFCAAt, the PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in: (1) mainland China of the People’s Republic of China because of a position taken by one or more authorities in mainland China; and (2) Hong Kong, a Special Administrative Region and dependency of the PRC, because of a position taken by one or more authorities in Hong Kong. In addition, the PCAOB’s report identified the specific registered public accounting firms which are subject to these determinations. Our registered public accounting firm, KPMG Huazhen LLP, is headquartered in mainland China or Hong Kong and was identified in this report as a firm subject to the PCAOB’s determination. On December 15, 2022, the PCAOB Board determined that the PCAOB was able to secure complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong and voted to vacate its previous determinations to the contrary. However, whether the PCAOB will continue to be able to satisfactorily conduct inspections of PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong is subject to uncertainties and depends on a number of factors out of our and our auditor’s control. The PCAOB continues to demand complete access in mainland China and Hong Kong moving forward and is making plans to resume regular inspections in early 2023 and beyond, as well as to continue pursuing ongoing investigations and initiate new investigations as needed. The PCAOB has also indicated that it will act immediately to consider the need to issue new determinations with the HFCAA if needed. If the PCAOB is unable to inspect and investigate completely registered public accounting firms located in China and we fail to retain another registered public accounting firm that the PCAOB is able to inspect and investigate completely in 2023 and beyond, or if we otherwise fail to meet the PCAOB’s requirements, our Class A ordinary Shares will be delisted from Nasdaq and will not be permitted for trading over the counter in the United States under the HFCAA and related regulations. On December 2, 2021, the SEC adopted final amendments implementing the disclosure and submission requirements under the Holding Foreign Companies Accountable Act, pursuant to which the SEC will (i) identify an issuer as a “Commission-Identified Issuer” if the issuer has filed an annual report containing an audit report issued by a registered public accounting firm that the PCAOB has determined it is unable to inspect or investigate completely because of the position taken by the authority in the foreign jurisdiction and (ii) impose a trading prohibition on the issuer after it is identified as a Commission-Identified Issuer for three consecutive years. See “Risk Factors — The recent enactment of the Holding Foreign Companies Accountable Act may result in de-listing of our securities.”

As a holding company, we may rely on dividends and other distributions on equity paid by our PRC subsidiaries for our cash and financing requirements. If any of our PRC subsidiaries incurs debt on its own behalf in the future, the instruments governing such debt may restrict their ability to pay dividends to us. As at the date of this prospectus, neither of our direct wholly or non-wholly owned subsidiaries nor the VIEs have made any dividends or other distributions to our holding company and the holding company has not made any dividends or distributions to any investors including U.S. investors as of the date of this prospectus. The holding company, its subsidiaries, and VIEs do not have any plan to distribute dividend or settle amounts owed under the prior or current contractual agreements in the foreseeable future. However, to the extent cash/assets in the business is in PRC/Hong Kong or our PRC/Hong Kong entity, the funds/assets may not be available to fund operations or for other use outside of the PRC/Hong Kong due to interventions in or the imposition of restrictions and limitations on the ability of us, our subsidiaries or the VIEs by the PRC government to transfer cash/assets. See “Transfer of Cash Through our Organization”, and “Risk Factors–Risks Related to Doing Business in China and Hong Kong — PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay us from using part of the proceeds of this offering to make loans or additional capital contributions to our PRC subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand our business” and “Restrictions on currency exchange may limit our ability to utilize our revenues effectively.” In the future, cash proceeds raised from overseas financing activities, including this offering, may be transferred by us to our PRC subsidiaries via capital contribution or shareholder loans, as the case may be. We currently don’t have any cash management policies and procedures in place that dictate how funds are transferred through our organization. Rather, the funds can be transferred in accordance with the applicable PRC laws and regulations. As of the date of this prospectus, no cash transfer has been made among the holding company, its subsidiaries and VIE.

Before buying any shares, you should carefully read the discussion of material risks of investing in our Class A Ordinary Shares in “Risk Factors” beginning on page 32 of this prospectus.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

|

PER SHARE |

TOTAL |

|||||

|

Initial public offering price |

$ |

$ |

||||

|

Underwriting discounts and commissions(1) |

$ |

$ |

||||

|

Proceeds, before expenses, to us |

$ |

$ |

||||

____________

(1) For a description of compensation payable to the underwriter, see “Underwriting” beginning on page 175.

We expect our total cash expenses for this offering (including cash expenses payable to our underwriters for their out-of-pocket expenses) to be approximately $[ ], exclusive of the above discounts and commissions. In addition, we will pay additional items of value in connection with this offering that are viewed by the Financial Industry Regulatory Authority, or FINRA, as underwriting compensation. These payments will further reduce proceeds available to us before expenses. See “Underwriting.”

This offering is being conducted on a firm commitment basis. The underwriters are obligated to take and pay for all of the shares if any such shares are taken. We have granted the underwriters an option for a period of forty-five (45) days after the closing of this offering to purchase up to 15% of the total number of our Class A Ordinary Shares to be offered by us pursuant to this offering (excluding shares subject to this option), solely for the purpose of covering over-allotments, at the initial public offering price less the underwriting discounts and commissions. If the Underwriter exercises the option in full, the total underwriting discounts and commissions payable will be $[ ] based on an assumed initial public offering price of $[ ] per Class A Ordinary Shares, and the total proceeds to us, before expenses, will be $[ ]. If we complete this offering, net proceeds will be delivered to us on the closing date.

The underwriters expect to deliver the Class A Ordinary Shares against payment as set forth under “Underwriting”, on or about , 2022.

Lead Underwriters

|

CMB INTERNATIONAL |

The Benchmark Company |

The date of this prospectus is , 2022.

|

Page |

||

|

1 |

||

|

32 |

||

|

77 |

||

|

78 |

||

|

79 |

||

|

80 |

||

|

81 |

||

|

83 |

||

|

85 |

||

|

89 |

||

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

91 |

|

|

109 |

||

|

112 |

||

|

127 |

||

|

139 |

||

|

146 |

||

|

148 |

||

|

152 |

||

|

167 |

||

|

169 |

||

|

175 |

||

|

185 |

||

|

186 |

||

|

186 |

||

|

187 |

||

|

190 |

||

|

F-1 |

We are responsible for the information contained in this prospectus and any free writing prospectus we prepare or authorize. We have not, and the underwriters have not, authorized anyone to provide you with different information, and we and the underwriters take no responsibility for any other information others may give you. We are not, and the underwriters are not, making an offer to sell our Class A Ordinary Shares in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front cover of this prospectus, regardless of the time of delivery of this prospectus or the sale of any Class A Ordinary Shares.

For investors outside the United States: Neither we nor the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction, other than the United States, where action for that purpose is required. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the Class A Ordinary Shares and the distribution of this prospectus outside the United States.

We are incorporated under the laws of the Cayman Islands and a majority of our outstanding securities are owned by non-U.S. residents. Under the rules of the U.S. Securities and Exchange Commission, or the SEC, we currently qualify for treatment as a “foreign private issuer.” As a foreign private issuer, we will not be required to file periodic reports and financial statements with the Securities and Exchange Commission, or the SEC, as frequently or as promptly as domestic registrants whose securities are registered under the Securities Exchange Act of 1934, as amended, or the Exchange Act.

Until and including , 2022 (twenty-five (25) days after the date of this prospectus), all dealers that buy, sell or trade our Class A Ordinary Shares, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

i

CONVENTIONS THAT APPLY TO THIS PROSPECTUS

Unless we explicitly state otherwise or the context otherwise indicates clearly, all references in this prospectus to “we,” “us,” “our,” “our Group,” or “the Group” refer to DDC Enterprise Limited and its subsidiaries.

The “Company” or “DDC Cayman” refers to DDC Enterprise Limited.

“HKD” or “HK$” refers to the legal currency of Hong Kong.

“Hong Kong” refers to Hong Kong Special Administrative Region of the People’s Republic of China.

“Macau” refers to Macau Special Administrative Region of the People’s Republic of China.

“RMB” or “Renminbi” refers to the legal currency of China.

“mainland China,” “PRC” or “China” refers to the People’s Republic of China, excluding, for the sole purpose of this prospectus, Hong Kong, Macau and Taiwan, unless the context otherwise indicates.

“Prospectus” refers to the public offering prospectus unless we explicitly state otherwise or the context otherwise indicates clearly.

“$” or “U.S. dollars” or “USD” refers to the legal currency of the United States.

We have made rounding adjustments to some of the figures included in this prospectus. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them.

Unless the context indicates otherwise, all information in this prospectus assumes no exercise by the underwriters of their over-allotment option and no exercise of the Underwriter Warrants.

Our business is primarily conducted in China, and the financial records of our subsidiaries in Asia are maintained in USD, and our functional currency is USD. Our consolidated financial statements are presented in U.S. dollars. We use U.S. dollars as the reporting currency in our consolidated financial statements and in this prospectus.

TRADEMARKS, SERVICE MARKS AND TRADE NAMES

This prospectus includes trademarks, tradenames and service marks, certain of which belong to us, including the DayDayCook logo, and others that are the property of other organizations. Solely for convenience, the trademarks, service marks, logos and trade names referred to in this prospectus are without the ® and ™ symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, service marks and trade names.

This prospectus contains additional trademarks, service marks and trade names of others, which are the property of their respective owners. All such trademarks, service marks and trade names appearing in this prospectus are, to our knowledge, the property of their respective owners. We do not intend our use or display of other companies’ trademarks, service marks, copyrights or trade names to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

ii

PUBLIC OFFERING PROSPECTUS SUMMARY

The following summary highlights information contained elsewhere in this prospectus and does not contain all of the information you should consider before investing in our Class A Ordinary Shares. You should read the entire prospectus carefully, including “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our consolidated financial statements and the related notes thereto, in each case included in this prospectus. You should carefully consider, among other things, the matters discussed in the section of this prospectus titled “Business” before making an investment decision. This prospectus contains information from an industry report commissioned by us and prepared by Frost & Sullivan, an independent research firm, to provide information regarding our industry. We refer to this report as the Frost & Sullivan Report.

Our Mission

Our mission is to inspire others to enjoy cooking as part of a quality lifestyle and culture. We are driven to improve lives by creating easy-to-cook, delicious, and healthy meal solutions. It is our vision to create fun experiences and inspirations in every kitchen.

Overview

We are a leading content driven (i.e. using content to reach and engage target customers) consumer brand offering easy, convenient ready-to-heat (“RTH”), ready-to-cook (“RTC”) and plant-based meal products (i.e. meal products consisting largely or solely of vegetables, fruits, grains and other foods derived from plant-based protein, rather than animal protein) while promoting healthier lifestyle choices to our predominately Millennial and Generation Z (“GenZ”) customer-base. We are also engaged in the provision of advertising services. Our business can be broadly divided into two main segments: (1) merchandise segment which includes sales of RTC, RTH, plant-based meal products, private label products, revenues from collaborative arrangements and advertising service; and (2) fresh products segment which includes fresh products sold to supermarkets and other third parties.

We were founded in Hong Kong in 2012 by Ms. Norma Ka Yin Chu, a highly regarded entrepreneur and a true cooking enthusiast, as an online platform which distributed food recipe and culinary content. Subsequently, we further expanded our business to provide advertising services to brands that wish to place advertisement on our platform or video content. In 2015, we entered the Mainland China market through the establishment of Shanghai DayDayCook Information Technology Co., Ltd (“SH DDC”) to engage in technology development of computer software, food circulation and advertising production in China. We pivoted our business in 2019 to include the production and sale of, among others, own-branded RTH, RTC and plant-based food products.

As of June 30, 2022, our main product categories include (i) own-branded RTH products — typically pre-or-semi-cooked meals with some but minimal preparation required ahead of serving, (ii) own-branded RTC products — ready to be consumed within 15 to 20 minutes with some additional cooking preparation, and (iii) plant-based meal products localized for the palate of a Chinese consumer, and (iv) private label products (i.e. third-party branded food products).

Business Model

Our omni-channel (online and offline) sales, end-to-end (“E2E”) product development and distribution strategy, and data analytics capabilities enable us to successfully identify, assess, and pivot to cater to changing consumer preferences and trends across multiple customer segments and price-points. From a product distribution standpoint, we have created a network of direct-to-customer (“D2C”), retailer, and wholesaler sale options.

• We leverage (i) large China-based e-commerce platforms e.g., Tmall, JD.com, Pinduoduo, (ii) leading livestreaming, video-sharing, content-marketing platforms e.g., ByteDance (TikTok and sister-app Douyin), Bilibili, Weibo, Little Red Book (小红书), Kuaishou etc., and (iii) online-merged-offline (OmO) group-buy platforms e.g., Meituan-Dianping to drive online sales. We would cooperate with third-party online distributors on these e-commerce platforms to promote and sell our products.

• We have access to a network of offline point-of-sales (“POS”) through partnerships with (i) convenience stores e.g., 7/11, Lawson etc., (ii) multi-national retail corporations e.g., Carrefour, Hema etc., (iii) boutique supermarket chains e.g., Ole’, G-Super etc., and (iv) various corporate partnerships e.g., Towngas to distribute and sell our products.

1

As of June 30, 2022, we had 20.3 million paid customers. Of the followers from social media & video platforms, around 70% are GenZ, 50% of customers are from East & South China, and 87% are female. In particular, we believe that our products appeal to GenZ because (1) when compared to older age groups, GenZ generally do not want to spend a long time cooking at home and they value cost effective options like RTC and RTH meals due to the ease of cooking that RTC and RTH products provide; (2) we promote our products mainly through social media, the audience of which are mainly the GenZ population; (3) we mainly sell our products through e-commerce platforms, including livestreaming e-commerce, the customers demographics of which are dominated by GenZ; (4) plant-based diets have progressed from a food trend to a globally recognized lifestyle which GenZ is more willing to embrace. The average age of a viewer engaging with our products or marketplace is younger than 30 years old. From 2018 to June 2022, we have a content library with more than 229,093 minutes of in-house created content.

For the year ended December 31, 2021, we recorded RMB205.2 million (or US$32.2 million) in total revenue, representing an increase of 21.3% when compared with the year ended December 31, 2020. Our focus has been on improving the overall cost structure of the business when facing Covid and inflation challenge. As a result, for the year ended December 31, 2021, our gross profit margin slightly increased to 17.8% versus 16.5% for the year ended December 31, 2020.

We had recurring losses from operations, net cash used in operating activities, net current liabilities and an accumulated deficit. In addition, our auditor’s report includes an explanatory paragraph expressing substantial doubt about our ability to continue as a going concern.

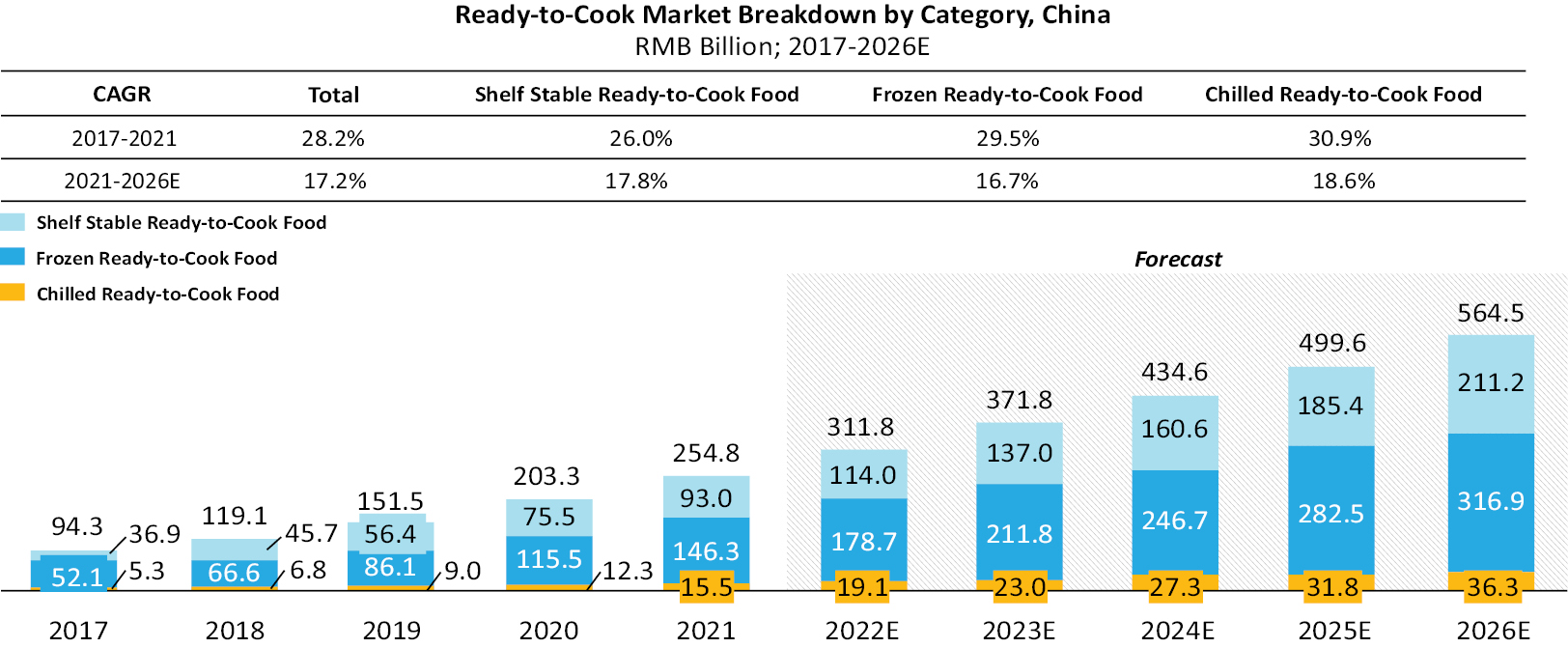

Our Industry

We compete primarily in the RTC, RTH and plant-based meat food products markets in China. With (i) the proliferation of food delivery service options, (ii) a shift in customer preference and behavior away from home-cooked to convenience, and (iii) an increase in GDP per capita/overall disposable income (both in our target demographic and in-general) the demand for RTC/RTH products has increased significantly. Customers have also become more discerning and expect RTC/RTH products to be of a high quality, have a higher nutritional value, and taste better when compared with other processed or semi-processed food product categories. Typically, RTC meals are made using high-quality and seasonal ingredients with full traceability at every stage of the food chain and a focus on nutritional value and maintaining a balanced diet is factored into the recipe and product R&D process.

COVID-19 has accelerated the shift to e-commerce and the need to develop and professionalize China’s cold chain transport infrastructure. The logistics industry is benefiting from the proliferation of professional third-party logistics service providers as well as improvements in preservation/storage, information logistics, analysis, and distribution technology. As a result of improvements in logistical infrastructure and the scale of the distribution network, the RTC industry has been able to expand its geographical reach, improve product delivery efficiency, and guarantee food safety and maintain quality over larger distances.

Internationally, the development history of mature overseas RTC markets nurtures an extensive customer base of RTC products. The COVID-19 pandemic further stimulates such demands in overseas markets as it alters people’s lifestyle and arouse health consciousness, especially in Southeast Asia, to a great extent. In addition, with the development of those mature RTC markets, an increasing number of customers are in pursuit of a healthier lifestyle

2

and start to favor healthier ready-to-cook products instead of RTC products of high calories. Chinese companies in the RTC industry, attributable to their well-established value chains, are able to offer RTC products of competitive prices in markets like North America and Europe despite the additional logistic expenses. Thus, Chinese companies that are actively seeking international expansion opportunities are well positioned to further gain share in the global RTC market.

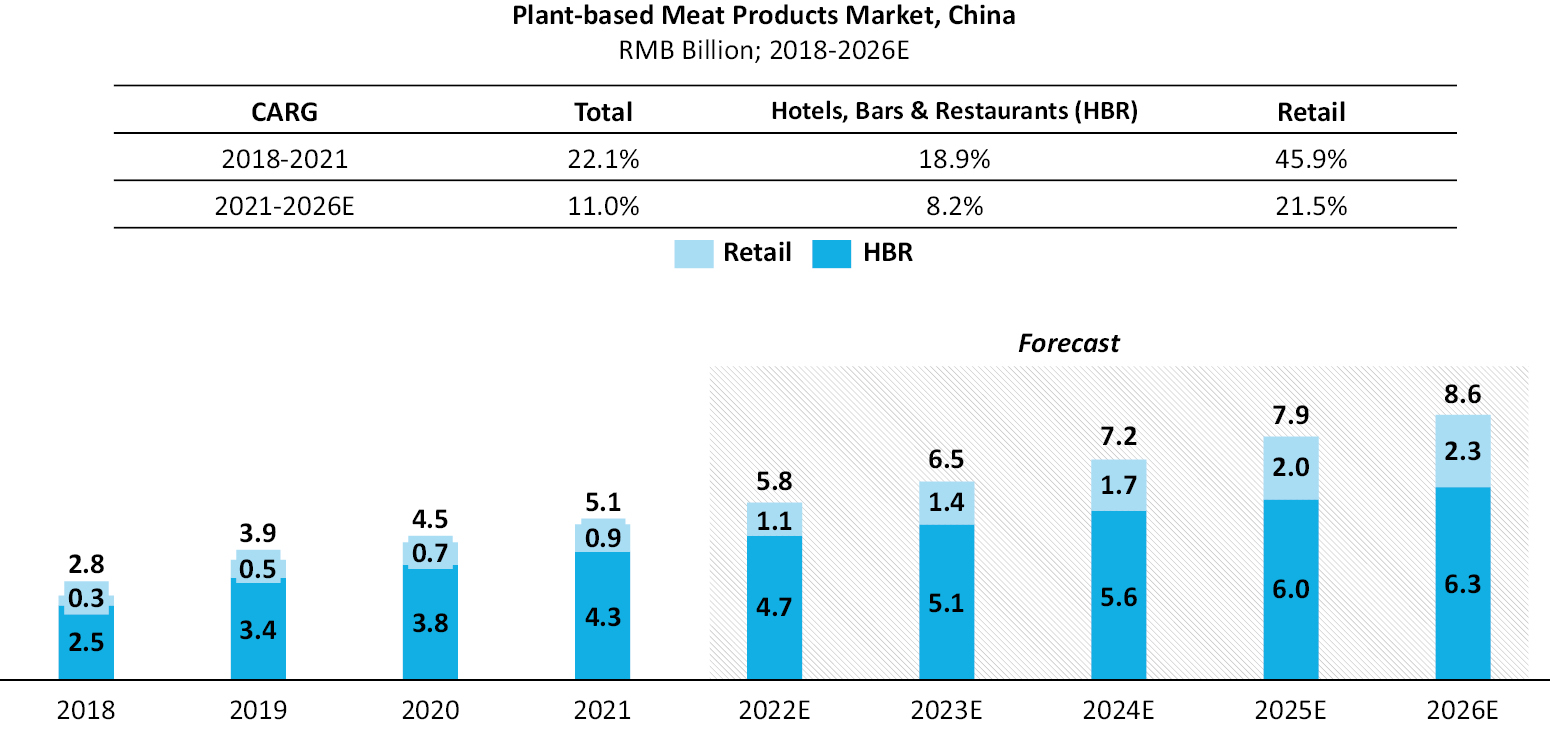

Plant-based products are a nascent Fast-Moving Consumer Goods (“FMCG”) category in China. Some Chinese brands have recently emerged as strong competitors to the more international incumbents. Younger individuals are the target demographic of companies offering plant-based substitutes/alternatives. Many new brands have been able to penetrate the younger customer segment by adopting an omnichannel strategy and by offering good quality, varied product offerings at a reasonable price-point.

Around the globe, the public has been paying more attention to environmental and natural resources protection over the past decades. The technology and production of plant-based meat have also experienced rapid development. Benefiting from the mature production technology of plant-based meat, foreign brands, when compared with Chinese brands, have obvious advantages in imitation of meat flavor and texture. However, limiting to product categories, flavor localization, stock-keeping unit (“SKU”) quantity, and high price, it is difficult for them to seize great business opportunities in Chinese market. Compared to foreign brands, domestic brands pay more attention to the recipe R&D and introduce various plant-based meat food products into the market, covering from Western cuisine to Chinese cuisine, including but not limited to Panini, pizza, hamburgers, braised rice, pies, noodles, and other products to cater consumers. Last but not least, the processed volume of soybean protein and pea protein in China contributes nearly half of the global volume every year, which provides a significant advantage in raw materials for domestic plant-based meat food products companies.

Our Competitive Strengths

We believe the following competitive strengths differentiate us from our competitors and will continue to contribute to our success:

Leading Content Driven Consumer Brand in China that Possess Loyal Customer Base, and Clear Alignment with Consumer Trends

We are a leading content-driven lifestyle brand for young food lovers, especially GenZ customers in China. We believe that our RTH, RTC, and plant-based meal products portfolio aligns with broader FMCG trends and shifts in consumer behavior. Our products, brand, and mission resonate strongly with our GenZ customer base who seek high quality, nutritional food products that are sustainably and ethically sourced. In the first half of 2022, we served 4.7 million D2C customers, a decrease at 8% Year-over-Year (“YoY”) was due to the lock down impact from COVID-19. As of June 30, 2022, more than 20.3 million consumers had purchased our products via one or more e-commerce platforms.

We produce culinary and lifestyle content (e.g., in short/long-form video and livestreaming formats) across major social media platforms garnering 300-450 million views per month.

Track Record of Innovation

We allocated and will continue to allocate significant resources to product innovation for our RTC and RTH products. We typically launch new products on a quarterly basis. To position us as a leader in the plant-based RTC and RTH categories, we partnered with PFI Foods in the third quarter of 2020 and cooperated with Meta Meat in 2021, both companies being leading plant-based meat manufacturers in mainland China, to develop a line of plant-based food products. We also recently invited Mr. Malik Sadiq PhD, the Chief Operating Officer of LIVEKINDLEY Co., a collective plant-based heritage and start-up brand to join as our advisor.

As of June 30, 2022, 32 active SKUs came from our product innovation. Of the 32 SKUs, 14 were plant-based products, 7 RTC, and 11 RTH. We plan to release a total of 19 SKUs in 2022, with 70% being plant-based products. In addition, we have built a library of over 9 new product concepts and recipes (co-brand collaboration with Nestle and Oatly), ready for further development and testing. We believe that we excel at identifying spice, ingredient combinations, and flavor profiles that appeal to the palate of Chinese consumers. Leveraging our innovation

3

capabilities, our experience in the Chinese markets and our deep understanding of the palate of Chinese consumers, we are confident that when executing our international market expansion plan, we can introduce new product innovation and develop food products that appeal to overseas Asians.

Omni-Channel and Multi-Faceted Sales & Distribution Strategy

Our omni-channel (both offline and online) strategy spans (i) popular e-commerce channels e.g., Taobao and JD.com, (ii) social and content platforms e.g., TikTok, Kuaishou, Bilibili, and WeChat, and (iii) community group buying platforms e.g., Meituan-Dianping. From 2019 to June 2022, our online sales network included, among others, Tmall, JD.com, China Pinduoduo have attracted 90.85 million visitors and for the year ended December 31, 2021, generated online consumer product sales of RMB148.6 million (or US$23.3 million) in online consumer product sales. In 2021, we increased our offline retail distribution network from 300 POS to access to approximately 4,000 POS. As of June 30, 2022, our offline retail distribution network covered a total of 4,137 POS.

We will accelerate our offline retail-partner expansion strategy going forward. We plan to gain access to an additional 5,000 POS in the short-to-medium term. Our multi-channel approach means we can adopt a highly differentiated pricing model and strategy by platform, distribution channel, product category, and across non-tier 1 cities in China. We target to build a network of POS location over 10,000 by the end of 2023.

Customer Engagement Analytics, Customer Service, and Real-Time (“RT”) Feedback Capabilities

We analyze transaction data, collect customer feedbacks through one or more channels, and engage in customer engagement analytics. This helps to (i) streamline the product development lifecycle and reduce the risk of a customer-product mismatch, (ii) uncover new (sub) product categories and/or potential bundling and/or up and cross-sell opportunities within the existing product portfolio, (iii) strengthen our brand image, and (iv) improve customer “stickiness” by providing customers with a forum.

4

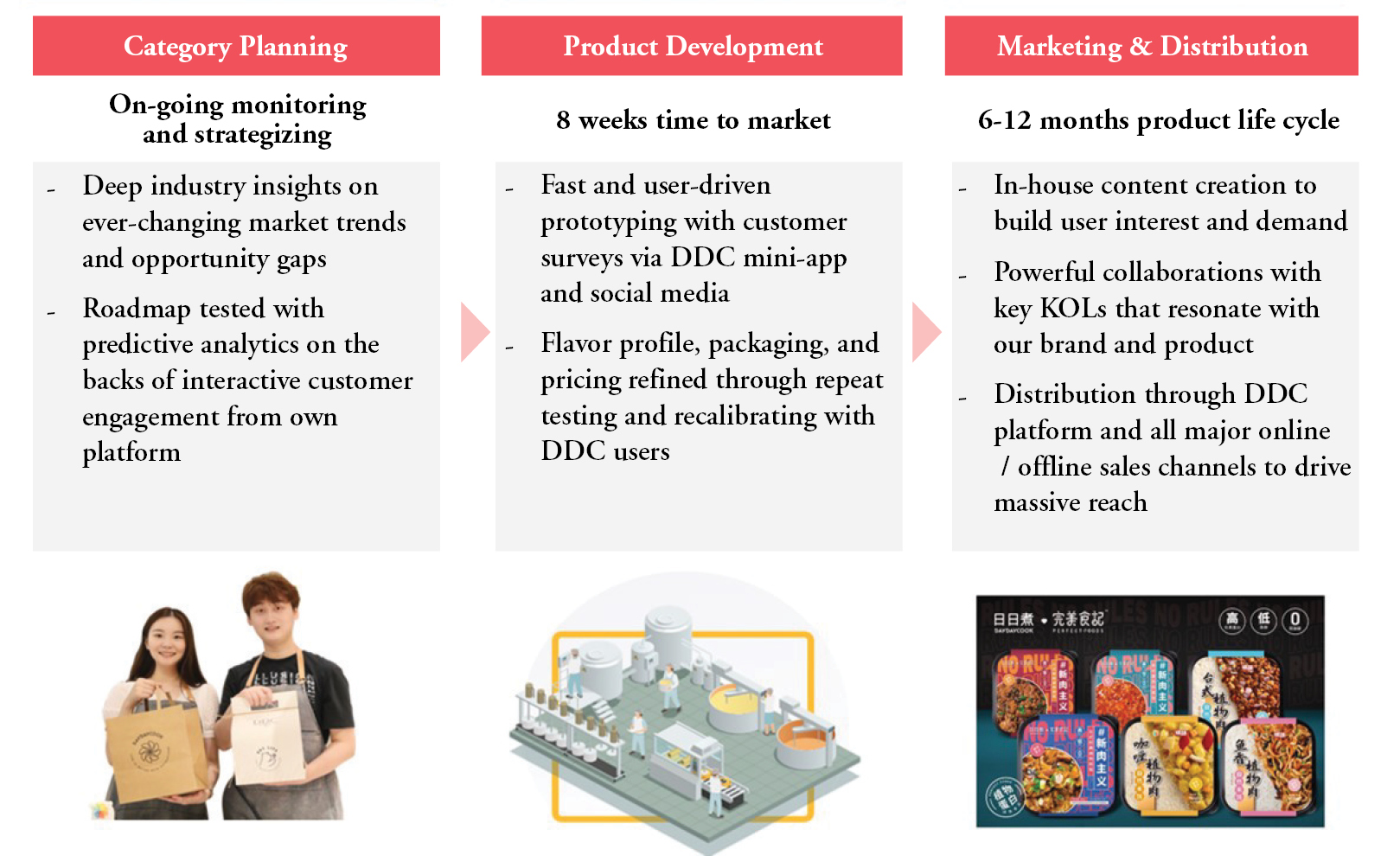

E2E Supply Chain Visibility, Agile Product Development and & Go-to-Market (“GTM”) Capabilities

On average, we can deliver a new product to-market within 8 weeks. Our E2E supply chain visibility and strong product execution i.e., product concept, prototyping, product validation and recalibration, commercial manufacturing, product marketing and placement capabilities means we can react almost real-time to changes in customer needs and preferences. As part of our more proactive new product development strategy, we leverage our deep industry and cross-disciplinary expertise to uncover potential market and product opportunities. We have an in-house content development team which focuses on building interest and demand pre product launch. They will keep abreast of latest market developments and identify latest potential trends and consumers interests. To promote our new products, we also collaborate with key opinion leaders (“KOLs” or “KOL”). We are well placed to continue to grow our market share and become the dominant player in the RTC, RTH food and plat-based meal products industry in China.

5

Experienced Management Team, Board of Directors, and Advisory Network

We have an experienced management team. Members of our management team have significant experience across the FMCG, e-commerce, and IT services/technology, media, and telecommunications industries/sectors.

In particular, our founder, Ms. Norma Chu, is a highly regarded entrepreneur and a true cooking enthusiast who has won numerous awards as visionary entrepreneur in the cooking and lifestyle community. She was named as China New Media Top 100 people in 2016, and one of CY Zone’s Most Notable Female Entrepreneurs for three consecutive years from 2017 to 2019. In 2020, she was awarded the Outstanding ICT Women Awards 2020: Women Entrepreneur Category, Harper’s Bazaar The Visionary Woman 2020 and JESSICA Most Successful Women Award 2020 — Digital Women. Prior to founding our group, Norma was the Head of Research of HSBC Private Bank in Hong Kong. Therefore, not only does Ms. Chu have rich experience in the cooking and food products industry, she also has extensive experience in private equity, which together enable her to lead our group’s drive to become a leader in the market.

We further augmented the management team with a Board of Directors and an advisory network with significant operator expertise and experience spanning PepsiCo, General Mills, Danone and Meitu.

|

Name |

Previous Roles |

Description |

||

|

Conor Chia Hung Yang |

Tuniu Corp., AirMedia, Dangdang Inc., and Goldman Sachs Group, Inc. |

• Mr. Yang has over 30 years of experience in capital market across the US & China, held C-level positions at several US-listed Chinese TMT companies • Former CFO of Tuniu, 51Talk, DangDang and AirMedia. Previously, Mr. Yang was a banker at Goldman Sachs, Morgan Stanley & Lehman Brothers • Mr. Yang currently serves as an independent director of I-Mab (Nasdaq: IMAB), Ehang (Nasdaq:EH), and iQIYI (Nasdaq: QI). |

||

|

Matthew Gene Mouw Independent Director |

Danone S.A., Barilla Group, MARS Inc |

• Mr. Mouw has over 30 years of extensive experience in the food industry, both convenience driven products such as confectionary, water & biscuits as well as planned purchase driven products such as juices, pasta and ready meals • Former Regional President Asia, Africa, and Australia for Barilla SpA. and General Manager for Danone S.A., in China • Mr. Mouw has experience with both emerging markets ranging from China to Turkey to Russia as well as developed markets ranging from Australia to Japan and Korea |

||

|

Sam Shih |

PepsiCo, Inc., Red Bull GmbH, Accor S.A, and OYO Rooms |

• Mr. Shih has over 30 years of experience in food & hospitality industry in China. • Mr. Shih is currently a Partner and Chief Operating Officer of OYO Hotel Company, a unicorn start-up backed by Softbank in China. • Previously Mr. Shih has served as CEO of PepsiCo Investment (China) Ltd., Asia Pacific Managing Director for Red Bull Gmbh as well as Chairman and CEO of Accor Great China |

6

|

Name |

Previous Roles |

Description |

||

|

Malik Sadiq, PhD Advisory Board Member |

The LIVEKINDLY Company, Inc., Tyson Foods, Inc., Arthur Andersen LLP, and Hitachi Vantara |

• Mr. Sadiq has more than 25 years of experience in the food and strategy consulting industry in China, India, and the US • Mr. Sadiq is currently the COO of LIVEKINDLY Co, a collective of plant-based heritage and start-up brands including The Fry Family Food Co., LikeMeat, and LIVEKINDLY Media • Previous roles include several senior management positions at Tyson Foods, most notably, CEO India, COO China, and Head of Global Sourcing and Business Optimization as well the Vice President, Consumer Practice at Hitachi Consulting |

Our Strategies

International market expansion

Internationally, the development history of mature overseas RTC markets nurtures an extensive customer base of RTC products. The COVID-19 pandemic further stimulates such demands in overseas markets as it alters people’s lifestyle and arouse health consciousness, especially in Southeast Asia, to a great extent. Chinese companies in the RTC industry, attributable to their well-established value chains, are able to offer RTC products of competitive prices in markets like North America and Europe despite the additional logistic expenses. Thus, Chinese companies that are actively seeking international expansion opportunities are well positioned to further gain share in the global RTC market.

Moreover, around the globe, the public has been paying more attention to environmental and natural resources protection over the past decades. Compared to foreign brands, domestic Chinese brands pay more attention to the recipe R&D and introduce various plant-based meat food products into the market, covering from Western cuisine to Chinese cuisine, including but not limited to Panini, pizza, hamburgers, braised rice, pies, noodles, and other products to cater consumers. The processed volume of soybean protein and pea protein in China contributes nearly half of the global volume every year, which provides a significant advantage in raw materials for Chinese plant-based meat food products companies.

In view of the above and to the extent permitted due to our recurring losses from operations and an accumulated deficit, we are raising funds from investors for the purpose of expanding our business in the U.S. and Southeast Asia in hope of widening our customer base.

For the U.S., we have devised a three-fold strategy: (1) to launch our products through major Asian-focused online and offline sales channels, (2) to launch our direct-to-consumer stores on Amazon and our U.S. website by the end of 2022, and (3) to grow through acquisitions. Since July 2022, we have successfully gained access to the U.S. market through sales on Yamibuy.com, one of the largest Asia food e-commerce platforms headquartered in the U.S.. Currently, we are in negotiation with major online Asia food e-commerce platforms and selected major Asian supermarket chains for our DayDayCook U.S. launch in the first quarter of 2023. As for the Southeast Asian market, we are currently negotiating with local companies that would give us instant access to a growing customer base in the RTC and RTH meal markets.

Enhance our sales and marketing capabilities, as well as our sphere of influence

We will continue to monitor the performance of our e-commerce partners and platforms, adapt our product pricing strategy and offerings, and expand our fulfilment capabilities to support our revenue targets. We are raising funds from investors to deepen and broaden our existing partnerships and continue to expand cooperation with a wider network of influencers and KOLs to build our brand awareness. Also, we plan to engage more up-and-coming social e-commerce platforms to (i) drive higher traffic to our stores through more and closer collaborations; (ii) improve our ability to aggressively penetrate non-tier 1 cities and (iii) accelerate the growth of our paid customer base. In addition, we will continue to improve our sales and marketing capabilities and leverage the internet and various social media platforms to build brand awareness in non-Tier 1 cities in China. We will also engage content and social media marketing providers and platforms to drive an increase in average order value (“AOV”), repeat purchases, and to attract net-new users to our platform.

7

As of June 30, 2022, we had 20.3 million paid customers. By the end of 2022, we expect to have over 43 million paid customers. We also plan to increase our access to offline retail locations to 10,000+ in the short-to-medium term — 8,400+ convenience stores, 530+ supermarkets, 920+ social commerce POS locations, and 330+ high-end specialty grocery stores.

Continue to innovate and expand product offerings

We expect consumer demand for RTH, RTC, and plant-based meal products to not only persist, but to grow at an accelerated rate. We plan to leverage our deep industry expertise, data-informed consumer insights, and predictive analytics to identify meaningful consumer trends and then partner with and solicit product feedback from our customers to optimize and expand on our existing product portfolio. We are committed to strengthening our R&D and product development capabilities to improve our ability to innovate more effectively within our core product categories.

Mergers and Acquisitions (“M&A”) Rollup

M&A is a key growth strategy going forward. To the extent permitted due to our recurring losses from operations and an accumulated deficit, we will evaluate and opportunistically execute on strategic joint ventures (JV), potential investments and acquisition opportunities across the supply-chain with a focus on supplementing and/or complementing our existing products, sales channels, customer-base and/or allow us to optimize our existing supply chain management capabilities. Apart from executing acquisitions with considerations paid through share exchanges, we are also raising funds from investors to have an option to acquire companies through a mixture of cash and shares.

Multi-brand Strategy

We adopt a multi-brand strategy to build a portfolio of products that has distinct brand names. We believe this could encourage our growth in more market segments and conducive to building our overall brand awareness, as well as enlarging our customer base by appealing to different groups of customers. We acquired two brands and their sales channels in 2021, to further charge our medium-to-longer term growth potential by executing on multi-brand strategy. The brand “Mengwei” (with 200+ SKUs) focuses on affordable RTH products penetrating into non-tier 1 cities through PDD channel. The other brand “Yujiaweng” (with 400+ SKUs) focuses on seafood RTH products with its major sales channels covering both offline distribution & overseas network.

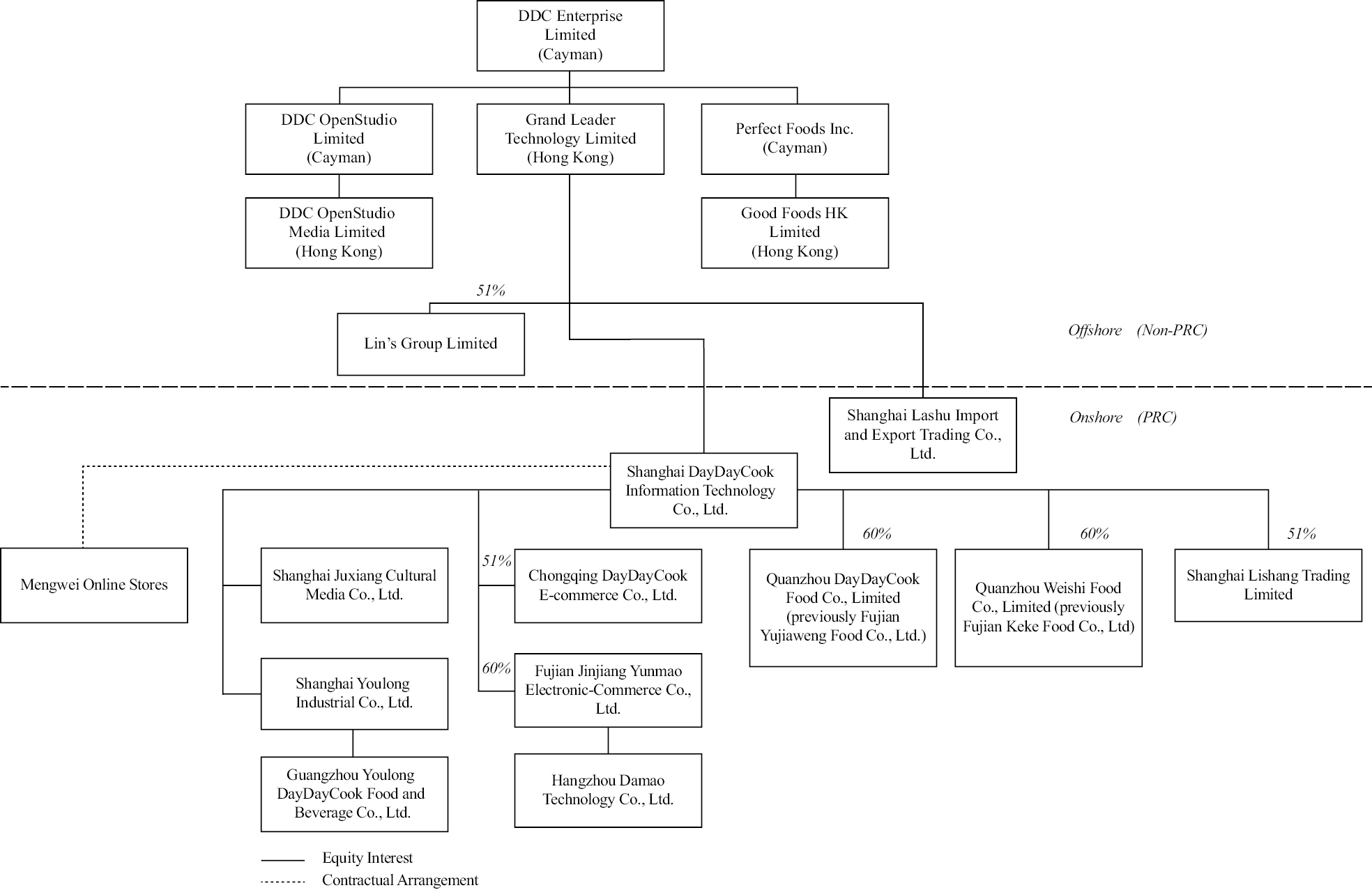

Corporate History and Structure

DDC Enterprise Limited (“DDC Cayman”) is a Cayman Islands holding company and conducts its operations primarily in China through its wholly-owned or controlled subsidiaries. We were founded in Hong Kong in 2012 by Ms. Norma Ka Yin Chu as an online platform which distributed food recipe and culinary content. Subsequently, we further expanded its business to provide advertising services to brands that wish to place advertisement on our platform or video content. In 2015, we entered the Mainland China market through the establishment of Shanghai DayDayCook Information Technology Co., Ltd. (“SH DDC”) and Shanghai Weishi Information Technology Co., Ltd. (“Weishi”). We pivoted our business in 2019 to include the production and sale of, among others, own-branded RTH, RTC and plant-based food products.

During the periods covered by the financial statements included elsewhere in this prospectus, SH DDC had entered into a series of contractual arrangement with Weishi and Shanghai City Modern Agriculture Development Co., Ltd. (“City Modern”), in 2017 and 2019 respectively, which allows SH DDC to exercise effective control over Weishi and City Modern and receive substantially all the economic benefits of Weishi, City Modern and their consolidated entities (collectively, the “Weishi and City Modern VIEs”) via variable interest entity structures. As of the date of this prospectus, such contractual arrangements with the Weishi and City Modern VIEs have been terminated. After the termination of the contractual arrangements with Weishi, we will continue cooperation with it in certain online service areas. For instance, Weishi will develop and maintain the WeChat mini-program related to our business, ensure the ordinary operation of our official websites, make sure the cyber security of the systems and maintain our IT systems and servers. As advised by the PRC legal adviser, our Company’s continue cooperation with Weishi does not constitute a VIE because that, since the termination of the contractual arrangements with Weishi, (i) our Company has no longer enjoyed any controlling rights or decision-making power over the operation of Weishi;

8

(ii) Weishi has independently operated its assets and properties and conducted its businesses, and its shareholder, instead of our Company, has enjoyed its residual interests and born the loss (if any); (iii) our Company and Weishi have no contractual relations other than the service contract signed between SH DDC and Weishi; and (iv) our Company has not enjoyed any interests or benefits, or any other transfers, contributed by Weishi, or offered any financial assistance for Weishi.

DDC Cayman directly and wholly owns (a) DDC OpenStudio Limited (“DDC OpenStudio”), a Cayman Islands company incorporated in May 2017, (b) Perfect Foods Inc. (“Perfect Foods Inc.”), a Cayman Islands company incorporated in September 2019 and (c) Grand Leader Technology Limited (“Grand Leader”), a Hong Kong company incorporated in January 2011. DDC OpenStudio in turn holds all the share capital of DDC OpenStudio Media Limited (“DDC OpenStudio Media”), which was incorporated in July 2018 in Hong Kong. Perfect Foods Inc. in turns holds all the share capital of Good Foods HK Limited (“Good Foods HK”), which was incorporated in September 2019 in Hong Kong.

Through its wholly-owned subsidiary Grand Leader, which was incorporated for the purpose of handling advertising, business-to-consumer e-commerce and cooking classes in Hong Kong, DDC Cayman owns a direct equity interest in SH DDC and Shanghai Lashu Import and Export Trading Co., Ltd. (“SH Lashu”). SH DDC was established in January 2015 in China for the purpose of engaging in technology development of computer hardware and software, food circulation and advertising production in China, whilst SH Lashu was established in August 2017 in China as an import and export vehicle in China.

As of December, 2017, Shanghai Youlong Industrial Co., Ltd. (“SH Youlong”), a wholly owned subsidiary of SH DDC, was established for the purpose of engaging in cooking class services, food and beverage and retail business in China. SH Youlong owns a direct equity interest in Guangzhou Youlong DayDayCook Food and Beverage Co., Ltd., which was established in March 2018 with its main business of engaging in cooking class services, food and beverage and retail business in China.

As of June 2019, Shanghai Juxiang Culture Media Co., Ltd. (“SH Juxiang”), a wholly owned subsidiary of SH DDC, was established for the purpose of engaging in e-commerce business in China.

As of January 2019, SH DDC acquired 60% equity interest in Fujian Jinjiang Yunmao Electronic Commerce Co., Ltd. (“Yunmao”), a limited liability company incorporated under the Laws of the PRC, for a combination of a share option consideration equivalent to a value of RMB10.2 million, and a cash consideration of RMB10.2 million, to engage in food and beverage retail and e-commerce. Yunmao owns a direct equity interest in Hangzhou Damao Technology Co., Ltd., which was established in June 2020 with a main business of e-commerce.

In January 2021, SH DDC acquired a number of online stores from Chongqing Mengwei Technology Co., Ltd., Liao Xuefeng, Chongqing Changshou District Weibang Network Co., Ltd. and Chongqing Yizhichan Snack Food Electronic Commerce Service Department (the “Transferors”). In July 2021, SH DDC and Chongqing Mengwei Technology Co., Ltd. set up a joint venture named Chongqing DayDayCook E-commerce Co., Ltd. (“CQ DDC”), which is established for accepting the online stores acquired and operating newly set-up online stores, in which, SH DDC holds 51% equity interest. CQ DDC was established for the purpose of engaging in online food retail business in China. However, due to certain limitations from the policies of third-party online platforms, the titles of such online stores currently cannot be transferred to CQ DDC and the operation of such online stores are still delegated to the Transferors through relevant contractual arrangements to enable us to have the ability to control such online stores. Therefore, these online stores are considered VIEs and SH DDC is the primary beneficiary. We refer to these online stores the “Mengwei VIE” throughout this prospectus. Investors should be aware that they are purchasing equity securities of our ultimate Cayman Islands holding company, namely DDC Cayman, rather than equity securities of the Mengwei VIE, and investors in our securities may never hold equity interests in the Mengwei VIE. DDC Cayman is a Cayman Islands holding company with no material operations of its own. The operations of online stores are conducted through contractual arrangements with the Transferors while other parts of our operations are conducted through our operating subsidiaries established in Hong Kong and mainland China. Although we took every precaution available to effectively enforce the contractual and corporate relationship with the Mengwei VIE, these contractual arrangements may still be less effective than direct ownership and that we may incur substantial costs to enforce the terms of the arrangements. For example, the Transferors, namely the operating agents of the Mengwei VIE, could breach their

9

contractual arrangements by, among other things, failing to conduct their operations in an acceptable manner or taking other actions that are detrimental to our interests. If we had direct ownership of the Mengwei VIE, we would be able to exercise our rights as a direct asset-holder to directly and effectively effect changes in the management and daily operation of the Mengwei VIE. However, under the current contractual arrangements, we rely on the performance of the Transferors of their obligations under the contracts to exercise control over the Mengwei VIE. The Transferors may not act in our best interests or may not perform their obligations under these contracts. In addition, failure of the Transferors to perform certain obligations could compel us to rely on legal remedies available under PRC laws, including seeking specific performance or injunctive relief, and claiming damages, which may not be effective or sufficient. All the agreements under the Mengwei VIE arrangements are governed by PRC law and provide for the resolution of disputes through arbitration in China. Accordingly, these contracts would be interpreted in accordance with PRC law and any disputes would be resolved in accordance with PRC legal procedures. The legal system in the PRC is not as developed as in some other jurisdictions, such as the United States. As a result, uncertainties in the PRC legal system could limit our ability to enforce these VIE agreements. The status of the rights of DDC Cayman, as a Cayman Islands holding company, with respect to the contractual arrangements with the Transferors is uncertain. Meanwhile, there are very few precedents and little formal guidance as to how contractual arrangements in the context of a VIE structure should be interpreted or enforced under PRC law. There remain significant uncertainties regarding the ultimate outcome of such arbitration should legal action become necessary. In addition, under PRC law, rulings by arbitrators are final, parties cannot appeal the arbitration results in courts, and if the losing parties fail to carry out the arbitration awards within a prescribed time limit, the prevailing parties may only enforce the arbitration awards in PRC courts through arbitration award recognition proceedings, which would require additional expenses and delay. In the event we are unable to enforce these VIE agreements for the Mengwei VIE, or if it suffers significant delay or other obstacles in the process of enforcing these VIE agreements, we may not be able to exert effective control over the Mengwei VIE, and our ability to conduct our business may be negatively affected.

On July 1, 2021, the Company, through its wholly owned subsidiary, Shanghai DayDayCook, entered into a purchase agreement (“the SPA”) with Mr. Zheng Dongfang and Mr. Han Min (“collectively the YJW Seller”), the shareholders of Fujian Yujiaweng Food Co., Ltd. (“Yujiaweng”) to acquire 60% interests of Yujiaweng’s product sales business, primarily including distribution contracts, the sales and marketing team, procurement team and other supporting function personnel (“the YJW Target Assets”). Yujiaweng is principally engaged in manufacturing and the distribution of snack foods. Shanghai DayDayCook and Mr. Zheng Dongfang agreed to form an entity (“YJW Newco”) with the Company holding 60% equity interest and Mr. Zheng Dongfang holding 40% equity interests. According to the SPA, during the period from July 1, 2021 until the date when YJW Newco is formed (“the transition period”), the Company manages and operates the Target Assets and is entitled to 60% of the net profit arising from the operation of the Target Assets.

On June 17, 2022, the YJW Newco, Quanzhou DayDayCook Food Co., Limited, was formed.

On July 1, 2021, the Company, through its wholly owned subsidiary, Shanghai DayDayCook, entered into a purchase agreement (“the SPA”) with Mr. Xu Fuyi, (“the KeKe Seller”), the shareholder of Fujian Keke Food Co., Ltd. (“KeKe”) and Mr. Zheng Dongfang, the president of KeKe, to acquire a 60% interest in KeKe’s product sales business, primarily including distribution contracts, the sales and marketing team, procurement team and other supporting function personnel (“the KeKe Target Assets”). KeKe is principally engaged in manufacturing and distribution of candy products. Shanghai DayDayCook and Mr. Zheng Dongfang agreed to form an entity (“KeKe Newco”) with the Company holding 60% equity interest and Mr. Zheng Dongfang holding 40% equity interests. According to the SPA, during the period from July 1, 2021 and the date when KeKe Newco is formed (“the transition period”), the Company manages and operates the Target Assets and is entitled to 60% of the net profit arising from the operation of the Target Assets.

On June 17, 2022, the KeKe Newco, Quanzhou Weishi Food Co., Limited, was formed.

As of April 2022, all contractual arrangements with Weishi and City Modern, have been terminated.

10

The following diagram illustrates our corporate structure as of the date of this prospectus. Unless otherwise indicated, equity interests depicted in this diagram are held 100%.

Government Regulations and Approvals for this Offering

As our operations are currently conducted through our operating entities established in Hong Kong and mainland China and we have VIE arrangements with various Chinese entities and individuals to enable us to have the ability to control a number of online stores, we are potentially subject to significant regulations by various agencies of the Chinese government. The Regulations on Mergers and Acquisitions of Domestic Companies by Foreign Investors, or the M&A Rules, adopted by six PRC regulatory agencies in 2006 and amended in 2009, require an overseas special purpose vehicle formed for listing purposes through acquisitions of PRC domestic companies and controlled by PRC companies or individuals to obtain the approval of the CSRC and Ministry of Commerce of the PRC (“MOFCOM”), prior to the listing and trading of such special purpose vehicle’s securities on an overseas stock exchange. Substantial uncertainty remains regarding the scope and applicability of the M&A Rules to offshore special purpose vehicles. As at the date of this prospectus, we have been advised by Grandall Law Firm (Shanghai) that CSRC’s approval under the M&A Rules is not required for the listing and trading of our Class A Ordinary Shares on [NYSE/Nasdaq] in the context of this offering given that (i) our PRC subsidiaries were incorporated as wholly foreign-owned enterprises by means of direct investment rather than by merger or acquisition of equity interest or assets of a PRC domestic company owned by PRC companies or individuals as defined under the M&A Rules that are DDC Cayman’s beneficial owners; (ii) we are a company incorporated under the laws of the Cayman Islands controlled by non-PRC citizens and we do not fit into the definition of “overseas special purpose vehicle” under the M&A Regulations; and (iii) the CSRC currently has not issued any definitive rule or interpretation concerning whether offerings like ours under this prospectus are subject to the M&A Rules. As such, we have never conducted any mergers or acquisitions of any PRC domestic companies with a related party relationship. MOFCOM’s approval under the M&A Rules is also not required as we have never conducted any mergers or acquisitions of any PRC domestic companies with a related party relationship. We cannot assure you that relevant PRC governmental agencies, including the CSRC, would reach the same conclusion as we do.

11

On July 6, 2021, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly issued the Opinions on Strictly Cracking Down on Illegal Securities Activities According to Law (the “Opinions”), which called for strengthened regulation over illegal securities activities and supervision on overseas listings by China-based companies and propose to take effective measures.

As at the date of this prospectus, no official guidance or related implementation rules have been issued in relation to the Opinions, and the interpretation and implementation of the Opinions also remain unclear to some extent at this stage. Based on our understanding of the current PRC laws and regulations in effect at the time of this prospectus, no prior permission is required under the M&A Rules or the Opinions from any PRC governmental authorities (including the CSRC) for consummating this offering by our company, except for the cybersecurity review from the CAC which we have applied for and completed as described in this Prospectus, as advised by our PRC legal adviser, Grandall Law Firm (Shanghai). However, there can be no assurance that the relevant PRC governmental authorities, including the CSRC, would reach the same conclusion as us, or that the CSRC or any other PRC governmental authorities would not promulgate new rules or new interpretation of current rules (with retrospective effect) to require us to obtain CSRC or other PRC governmental approvals for this offering. If we or our subsidiaries inadvertently conclude that such permission is not required, our ability to offer or continue to offer our Class A Ordinary Shares to investors could be significantly limited or completed hindered, which could cause the value of our Class A Ordinary Shares to significantly decline or become worthless. Our Group may also face sanctions by the CSRC, the CAC or other PRC regulatory agencies. These regulatory agencies may impose fines and penalties on our operations in China, limit our ability to pay dividends outside of China, limit our operations in China, delay or restrict the repatriation of the proceeds from this offering into China or take other actions that could have a material adverse effect on our business, financial condition, results of operations and prospects, as well as the trading price of our securities.

The PRC Data Security Law, which took effect on September 1, 2021, imposes data security and privacy obligations on entities and individuals that carry out data activities, provides for a national security review procedure for data activities that may affect national security and imposes export restrictions on certain data and information. On August 20, 2021, the Standing Committee of the National People’s Congress, or the SCNPC, promulgated the PRC Personal Information Protection Law (the “PIPL”), which took effect on November 1, 2021. The PIPL sets out the regulatory framework for handling and protection of personal information and transmission of personal information to overseas. The PRC regulatory requirements regarding cybersecurity are constantly evolving. For instance, various regulatory bodies in China, including the Cyberspace Administration of China, the Ministry of Public Security and State Administration for Market Regulation, or the SAMR, have enforced data privacy and protection laws and regulations with varying and evolving standards and interpretations. On November 14, 2021, the Cyberspace Administration of China, or the CAC, issued the Draft Cyber Data Security Regulations for public comments, pursuant to which, data processors carrying out the following activities must, in accordance with the relevant national regulations, apply for a cybersecurity review: (i) the merger, reorganization or spin-off of internet platform operators that possess a large number of data resources related to national security, economic development and public interests that affects or may affect national security; (ii) listing in a foreign country of data processors that process the personal information of more than one million users; (iii) listing in Hong Kong of data processors that affects or may affect national security; and (iv) other data processing activities that affect or may affect national security. The scope of and threshold for determining what “affects or may affect national security” is still subject to uncertainty and further elaboration by the CAC.

On December 28, 2021, the Cyberspace Administration of China (the “CAC”), and 12 other relevant PRC government authorities published the amended Cybersecurity Review Measures, which came into effect on February 15, 2022. The final Cybersecurity Review Measures provide that a “network platform operator” that possesses personal information of more than one million users and seeks a listing in a foreign country must apply for a cybersecurity review. Further, the relevant PRC governmental authorities may initiate a cybersecurity review against any company if they determine certain network products, services or data processing activities of such company affect or may affect national security. As a network platform operator who possesses personal information of more than one million users for purposes of the Cybersecurity Review Measures, we have applied for and completed the cybersecurity review with respect to our proposed overseas listing pursuant to the Cybersecurity Review Measures. As there remains significant uncertainty in the interpretation and enforcement of relevant PRC cybersecurity laws and regulations, we cannot assure you that we would not become subject to enhanced cybersecurity review or investigations launched by PRC regulators in the future. Any failure or delay in the completion of the cybersecurity review procedures or any other non-compliance with the related laws and regulations may result in rectification, fines or other penalties, including suspension of business, website closure, removal of our app from the relevant app stores, and revocation of prerequisite

12

licenses, as well as reputational damage or legal proceedings or actions against us, which may have material adverse effect on our business, financial condition or results of operations. See “Risk Factors — Risks Relating to Doing Business in China and Hong Kong — We may be liable for improper collection, use or appropriation of personal information provided by our customers.”

On December 24, 2021, the State Council published the draft Administrative Provisions on the Overseas Issuance and Listing of Securities by Domestic Companies (Draft for Comments) (the “Administrative Provisions”), and the CSRC published the draft Measures for Record-filings of the Overseas Issuance and Listing of Securities by Domestic Companies (Draft for Comments) (the “Administrative Measures”, collectively with the Administrative Provisions, the “Draft Rules Regarding Overseas Listing”), for public comment. It should be noted that neither the Administrative Provisions nor the Administrative Measures have come into effect as of the date of this registration statement.

Pursuant to the Article 2 of the Administrative Measures, domestic enterprises that directly or indirectly offer or list securities on an overseas stock exchange shall file with the CSRC. Our PRC subsidiaries are not “directly” offering securities overseas. Where an enterprise, whose principal business activities are conducted in China, seeks to issue and list its shares in the name of an overseas entity, such practice is deemed as an indirect overseas offering and listing. Among other things, if an overseas listed issuer intends to implement any offering in an overseas market, it should, through its major operating entity incorporated in the PRC, submit filing materials to the CSRC within three working days after the completion of the offering. According to the Administrative Measures, if the issuer meets the following conditions, it shall be deemed as an “indirect” overseas offering and listing of a domestic enterprise:

(1) the operating income, total profit, total assets or net assets of the domestic enterprise in the most recent fiscal year account for more than 50% of the relevant data in the issuer’s audited consolidated financial statements for the same period; and

(2) most of the senior management personnel responsible for business operation and management are Chinese Citizens or having an ordinary residence located in the PRC, and the principal place of business operation is located in or mainly within the PRC.

The Draft Rules Regarding Overseas Listing, if enacted, may subject us to additional compliance requirement in the future, and we cannot assure you that we will be able to get the clearance of filing procedures as required on a timely basis, or at all. Any failure of us to fully comply with new regulatory requirements may significantly limit or completely hinder our ability to offer or continue to offer our Class A ordinary shares, cause significant disruption to our business operations, and severely damage our reputation, which would materially and adversely affect our financial condition and results of operations and cause our Class A ordinary shares to significantly decline in value or become worthless.

Requisite Licenses and Approvals for Our Operations

Our business is subject to governmental supervision and regulation by the relevant PRC governmental authorities, including but not limited to the State Council, the SAMR, the Ministry of Commerce (the “MOFCOM”), the State Internet Information Office, the General Administration of Customs and other governmental authorities in charge of the relevant services provided by us. These government authorities promulgate and enforce regulations that cover various aspects of the operation of food products and e-commerce, including entry into these industries, scope of permitted business activities, licenses and permits for various business activities.